Are Solar Bonds A Good Investment?

If you’ve browsed the web recently and have a habit of reading up on finance, there’s a good chance you’ve seen an ad for an intriguing new investment: solar bonds. These ads, from energy provider SolarCity, certainly succeed in making their product sound attractive.

While it may seem like just another pop-up ad, the delivery of this investment is actually revolutionary. Marketers are reaching out to retail investors and offering “attractive returns” in an “investment that matters” for as little as $1,000 that can be set up in only 10 minutes!

I personally think the marketing is brilliant, but as we know, marketing doesn’t make a great investment. Let’s dig a little deeper.

Solar Bonds vs. Other Investments

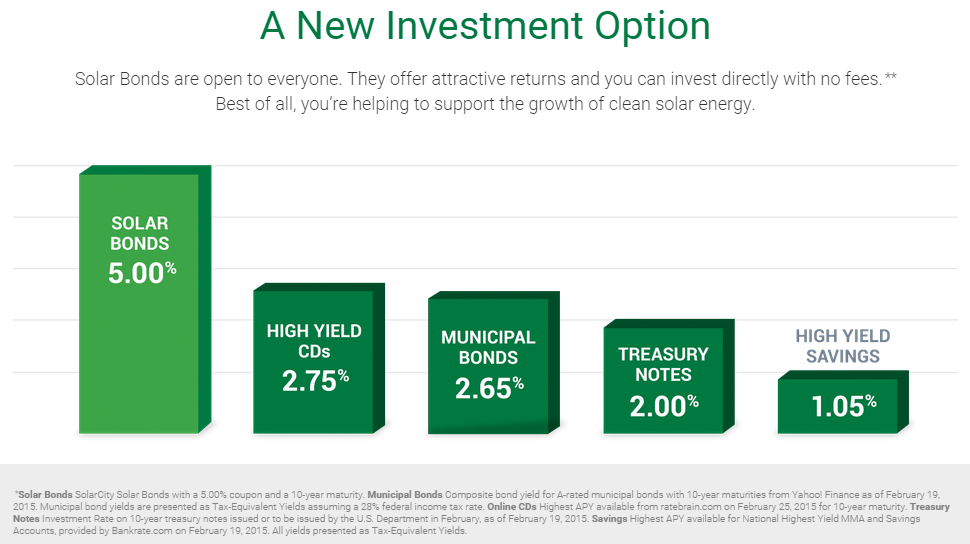

SolarCity’s website compares the solar bonds to CDs, Municipal Bonds, Treasury Notes and High Yield Savings accounts. In today’s low interest rate environment many investors are looking for income, which can be dangerous if not properly understood. When evaluating bonds you want to make sure you are compensated for term risk (how long you lend your money) and credit risk (the risk the company will default and not pay you back).

Do Solar Bonds Really Yield Attractive Returns?

The comparisons made on the SolarCity website are accurate, but not relevant given that the investments have different levels of term risk and/or credit risk. So are the returns attractive? When trying to determine the credit risk of the company I found this article stating S&P had assigned the third issue of SolarCity a rating of BBB+. It should be noted that the bond issue that was evaluated was secured by 15,915 panel systems, whereas the offering made to the general public is an unsecured obligation of SolarCity. Basically, you are left hoping SolarCity doesn’t default or go bankrupt.

To create a more apples-to-apples comparison, I searched for corporate bonds with a rating of BBB and a maturity near 15 years. Here is what I found:

| Issue | Moody Rating | S&P Rating | Coupon | Maturity | Category | YTM |

| NORTHWESTERN BELL TEL CO | Baa3 | BBB- | 7.75 | 5/1/2030 | Telephone | 6.762 |

| EL PASO ENERGY CORP MTN BE | Baa3 | BBB- | 8.05 | 10/15/2030 | Industrial | 6.856 |

| WILLIAMS COS INC DEL | Baa3 | BB+ | 7.5 | 1/15/2031 | Industrial | 6.692 |

| SOUTHERN NAT GAS CO | Baa3 | BBB- | 7.35 | 2/15/2031 | # | 6.417 |

| KINDER MORGAN ENERGY PARTNERS | Baa3 | BBB- | 7.4 | 3/15/2031 | Utility | 6.56 |

| PHELPS DODGE CORP | Baa2 | BBB- | 9.5 | 6/1/2031 | Industrial | 7.501 |

| WILLIAMS COS INC DEL | Baa3 | BB+ | 7.75 | 6/15/2031 | Industrial | 6.818 |

| EL PASO ENERGY CORP MTN BE | Baa3 | BBB- | 7.8 | 8/1/2031 | Industrial | 6.799 |

| ALBERTA ENERGY LTD | Baa2 | BBB | 7.375 | 11/1/2031 | Industrial | 6.47 |

| PANCANADIAN PETE LTD | Baa2 | BBB | 7.2 | 11/1/2031 | Industrial | 6.418 |

So why choose solar bonds? Essentially, you are able to invest in bonds of similarly rated companies with a yield to maturity of around 6.73%.

Elon Musk Invested $90 Million, So It Must Be Good!

If you do a quick internet search you’ll quickly see that SpaceX, founded by Elon Musk, invested $90 million in solar bonds — and they did so in mere minutes! To the many who look up to this widely-Internet-admired CEO, that may seem like proof enough that solar bonds constitute the resilient, promising, and futuristic investment they are proclaimed to be.

It should be noted, however, that Elon Musk is a 21% shareholder of Solar City, his cousin is one of the co-founders, and he is the company’s Chairman. It is therefore reasonable to assume that he might have other motives than return when making the investment – and, thus, this is not exactly a stable indicator of its promise for other investors.

Understand The Risk Involved

As with any area of investment, research is your friend. The questions I would ask before investing in solar bonds are simple:

First, “Why do they need to issue bonds?”

And, second, “Will they be able to repay me?”

When researching why they need to issue bonds, I came across two main explanations:

The business model is to lease or install solar panels, and the customer pays Solar City back over time. When reviewing the company’s balance sheet, it became apparent their total assets exceed total liabilities, but their receivables were only $23m (a small amount relative to the debt being issued).

SolarCity is not profitable. Although in the trailing twelve months, the company generated $259 million of revenue, net income was negative $59m. Solar City has had negative EBITDA every year of its existence. To put it simply, they need funding to stay in business.

In Conclusion

Even though 5.75% guaranteed interest seems attractive in today’s interest rate market, you should thoroughly understand the risks before investing into solar bonds. You may be able to get a greater yield from other bonds with similar risk profiles.

Fifteen years is a long time to loan money to a company that isn’t profitable, has only been in existence since 2009, and is trying to find its way as solar tax subsidies begin to phase out. If you do want to invest in high yield bonds such as these, understand they can be very volatile and you risk losing your entire principal by pursuing them. When investing in the high yield space, I always recommend massive diversification to mitigate the risks associated with concentrating in a single company.